In today’s complex world, navigating the nuances of insurance can feel overwhelming, especially when confronted with documents that seem technical and obscure. For many individuals, families, and businesses, understanding critical insurance documents is paramount to effective financial risk management. Today, let’s join DoctinOnline to find out about a document that frequently arises in contractual agreements and business dealings: the certificate of liability insurance form. This seemingly simple piece of pa, and why it’s a cornerstone of responsible financial planning and business operations.

What is a Certificate of Liability Insurance

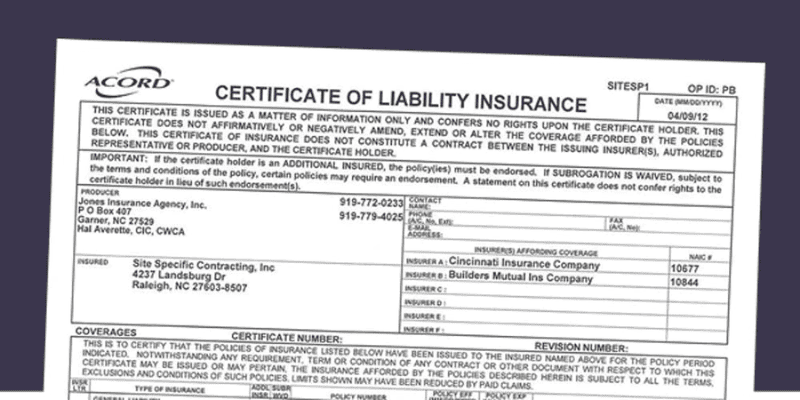

A certificate of liability insurance form is a formal document issued by an insurance company or its authorized agent, serving as proof that an insured party has a valid liability insurance policy in force. It acts as a concise summary of the policy’s key terms and conditions, rather than being the policy itself. This document confirms the existence of coverage, specifies the types of liability insured against, the policy limits, effective dates, and the insurance company providing the coverage. It is commonly requested by third parties who require assurance that the entity they are engaging with is financially protected against potential claims arising, it’s a quick and verifiable way to confirm insurance status without revealing the full, often extensive, policy document.

Purpose and significance

The primary purpose of a certificate of liability insurance form is to provide verification of insurance coverage to interested third parties. This typically includes clients, landlords, project owners, lenders, or regulatory bodies. For instance, a general contractor might require their subcontractors to provide a certificate of liability insurance before beginning work on a site. This protects the general contractor, rather than relying solely on the at-fault party’s personal assets.

Who needs this document

Various individuals and entities frequently need to either provide or request a certificate of liability insurance form. Businesses of all sizes,.

Key Components of the Certificate Form

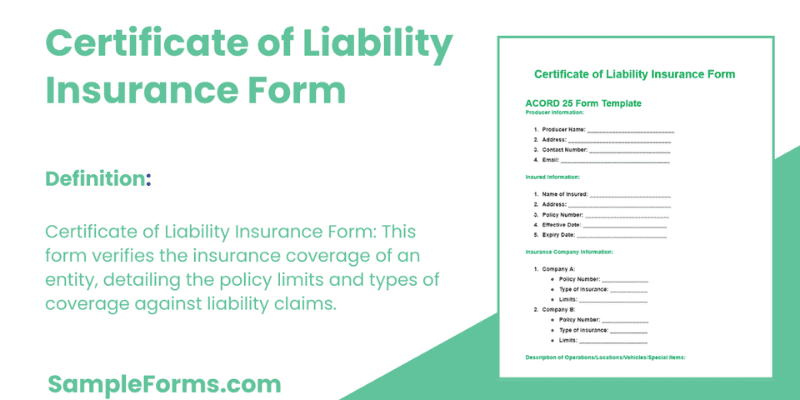

Understanding the information presented on a certificate of liability insurance form is crucial for both the party providing it and the party requesting it. While the specific layout may vary slightly, standard certificates, often using an ACORD form, contain several universal sections. These sections collectively paint a clear picture of the insurance coverage without delving into the exhaustive detail of the full policy. Familiarizing yourself with each part allows for a swift and accurate assessment of the protection offered. It ensures that the coverage meets the requirements of any contractual agreement or regulatory mandate, thereby preventing misunderstandings and potential gaps in risk management.

Understanding the basics

At the top of the certificate, you will typically find information identifying the insurance producer (the agent or broker who issued the certificate), the insurance company providing the coverage, and the policy number. Crucially, the “named insured” section clearly identifies the individual or entity covered by the policy. This is usually the business or person whose liability is being attested to. The “certificate holder” section, on the other hand, identifies the party requesting the certificate—the one who needs proof of insurance. It is important to verify that the named insured matches the party providing the service and that the certificate holder is correctly identified, especially if additional insured status is required, as this grants them specific protections under the policy.

Deciphering policy details and limits

One of the most critical sections details the types of coverage provided and their respective limits. For liability insurance, this usually includes Commercial General Liability (CGL), which covers bodily injury and property damage, and potentially other forms like professional liability (errors and omissions), auto liability, or umbrella liability. Each type of coverage will list aggregate limits (the maximum amount the insurer will pay for all claims during the policy period) and occurrence limits (the maximum amount for a single incident). The effective dates of the policy, including both the start and end dates, are also prominently displayed. Reviewing these limits and dates is paramount to ensure the coverage is adequate for the risks involved and that the policy is active for the duration it is needed. Any specific endorsements, such as “additional insured” clauses or waivers of subrogation, will also be noted, indicating expanded protection for the certificate holder.

Obtaining and Utilizing Your Certificate

For any individual or business, understanding how to obtain and effectively utilize a certificate of liability insurance form is an integral part of responsible operations. This document is not something you generate yourself; rather, it’s a formal communication.

The process of acquisition

Obtaining a certificate of liability insurance form is typically a simple process that begins with contacting your insurance agent or broker. You will need to provide them with specific information, including the name and address of the party requesting the certificate (the certificate holder), and any special requirements they might have, such as becoming an “additional insured” on your policy or specific coverage limits. Your agent will then generate the certificate based on your existing policy and send it directly to you or the requesting party. It’s important to request the certificate well in advance of when it’s needed, as processing times can vary, though many agents can issue them electronically within hours. Always double-check the details on the received certificate to ensure accuracy and completeness before forwarding it.

Common scenarios requiring presentation

The need to present a certificate of liability insurance form arises in numerous professional and personal contexts. Businesses, particularly those operating in high-risk industries like construction or manufacturing, will frequently provide these certificates to clients before commencing work. Landlords routinely require tenants, both commercial and residential, to furnish proof of liability coverage. Event organizers often demand certificates.

Beyond the Certificate: Policy Versus Form

It is absolutely critical to understand that a certificate of liability insurance form is merely a snapshot or summary of a larger, more comprehensive document: the actual insurance policy. While the certificate serves as convenient proof of coverage for third parties, it does not detail all the intricacies, exclusions, conditions, and endorsements contained within the full policy document. Misinterpreting the certificate as the complete policy can lead to significant misunderstandings and potentially expose parties to unforeseen risks. DoctinOnline consistently advises its readers to always refer to the actual policy for a full understanding of their coverage, and to not solely rely on the condensed information provided on the certificate.

The actual contract versus the summary

The full insurance policy is a legally binding contract between the insured and the insurance company, outlining all the terms, conditions, exclusions, and limitations of coverage. It can be a lengthy document, often dozens or even hundreds of pages long. In contrast, the certificate of liability insurance form is typically a single page designed for quick review. It confirms the existence of certain coverage types and limits but does not include the fine print of what is specifically excluded or the exact conditions that must be met for a claim to be valid. For example, a certificate might show general liability coverage, but the policy itself will detail specific exclusions for certain types of work, environmental damage, or intentional acts. Relying solely on the certificate can give a false sense of security regarding the actual scope of protection.

Important considerations for review

When you are the party requesting a certificate of liability insurance form, a thorough review is essential. Do not simply file it away; instead, carefully check several key aspects. Verify that the named insured is the correct party and that the certificate holder (you or your entity) is accurately listed, especially if “additional insured” status is required. Confirm that the policy effective dates cover the entire period of your engagement or project. Crucially, examine the coverage types and limits to ensure they meet the minimum requirements stipulated in your contract or risk management standards. If your agreement requires specific endorsements, such as a waiver of subrogation, ensure these are explicitly noted on the certificate. Any discrepancies or missing information should prompt an immediate inquiry with the issuing agent.

Protecting Your Interests and Managing Risk

In the realm of financial protection, proactive risk management is always the best strategy. Understanding and properly utilizing the certificate of liability insurance form is a fundamental aspect of this. Whether you are providing the certificate to assure others of your financial responsibility or requesting one to safeguard your own interests, diligent attention to detail is paramount. Beyond simply acquiring the document, a dee.

Assessing coverage adequacy

When reviewing a certificate of liability insurance form, one of the most critical steps is to assess whether the coverage limits are adequate for the potential risks involved. For instance, if you are a homeowner hiring a contractor for a major renovation, ensuring their general liability limits are substantial enough to cover extensive property damage or serious bodily injury is vital. In business, contract requirements often dictate minimum liability limits. However, even without specific mandates, a prudent risk manager will consider the scale and nature of the work, the potential for catastrophic loss, and industry benchmarks for appropriate coverage. Sometimes, basic limits may not be enough, and it might be advisable to request higher limits or supplementary umbrella coverage to truly mitigate significant financial exposure.

Best practices for businesses and individuals

For businesses, maintaining current and adequate liability insurance and being ready to provide a certificate of liability insurance form is a best practice. Regularly review your policies to ensure they align with your evolving operations and risk profile. Keep digital and physical copies of all certificates you issue and receive. For individuals engaging contractors or service providers, always request a certificate before work begins. Do not hesitate to contact the insurance agent listed on the certificate to verify its authenticity and confirm the details if you have any doubts. This due diligence can save considerable distress and financial loss down the line. Moreover, remember that the certificate only confirms coverage; understanding the full policy is what truly informs your risk exposure.

Conclusion

The certificate of liability insurance form is far more than just a piece of paper; it is a vital tool for financial risk management, providing essential proof of coverage and fostering trust in numerous transactions and partnerships. By understanding its components, its purpose, and the critical distinction between the certificate and the actual insurance policy, you can navigate your personal and professional dealings with greater confidence. DoctinOnline encourages you to leverage this knowledge to protect your interests effectively. For further guidance on selecting the right insurance products, analyzing policy benefits, and optimizing your risk management strategy, explore more of our comprehensive resources to make empowered decisions for your financial future.

{kind=link}