As a Senior Risk Manager and Insurance Consultant with over a decade of experience, I understand the profound importance of safeguarding your family’s financial future. For military families, this responsibility carries unique considerations, given the inherent risks and mobility associated with service. In this article, DoctinOnline will accompany you to explore the critical aspects of selecting the best life insurance companies for military families, providing the insights you need to make informed decisions. We aim to clarify complex policy details, compare market options, and offer practical advice to ensure you secure robust protection tailored to your distinctive circumstances.

The Unique Life Insurance Needs Of Military Families

Military families face distinct challenges and opportunities when it comes to life insurance. Unlike civilian occupations, military service involves potential deployments, combat exposure, and frequent relocations, all of which can impact insurance eligibility, policy terms, and premium rates. Understanding these unique needs is the first step toward building a comprehensive financial protection plan. Servicemembers’ Group Life Insurance (SGLI) and Family Servicemembers’ Group Life Insurance (FSGLI) offer foundational coverage for active-duty personnel and their families, providing up to $500,000 for service members and up to $100,000 for spouses, along with $10,000 for dependent children. While these government-sponsored programs are invaluable, they often serve as a baseline, and many military families require supplementary private coverage to adequately address their full financial obligations and long-term goals.

Moreover, the transition, and converting it to Veterans’ Group Life Insurance (VGLI) may come with higher costs as premiums are based on age, potentially making it less competitive over time. This emphasizes the need for portable policies that can continue regardless of service status. Factors such as a spouse’s income dependency, the presence of children, or ongoing financial obligations like mortgages necessitate a thorough evaluation of coverage beyond government provisions.

Key Factors When Choosing Life Insurance For Military Personnel

Selecting the right life insurance for military families involves a careful assessment of several critical factors. These go beyond standard considerations, delving into specific provisions that cater to the military lifestyle. Transparency and flexibility are paramount to ensure the policy remains effective throughout various stages of military service and beyond.

War Clauses And Deployment Coverage

A crucial distinction for military personnel is the presence or absence of “war clauses” or military service exclusion clauses in private life insurance policies. Many standard civilian policies may contain provisions that limit or deny benefits if death results.

Financial Strength Of The Insurer

The financial stability of a life insurance company is always a critical consideration, but it takes on added weight for long-term policies. Life insurance is a promise to pay a death benefit decades into the future, making the insurer’s ability to meet those obligations paramount. Independent rating agencies like AM Best, Fitch, Moody’s, and Standard & Poor’s assess insurance companies’ financial strength. An “A++” (Superior) rating. DoctinOnline always recommends opting for companies with consistently high financial strength ratings to ensure reliability and peace of mind for your family’s future.

Portability And Convertibility

Military careers often involve frequent moves and eventual transitions to civilian life. Therefore, the portability of a life insurance policy is highly advantageous. A portable policy remains in force regardless of changes in duty station or separation. Companies that offer generous conversion options provide greater flexibility and long-term security.

Top Life Insurance Companies Serving Military Families

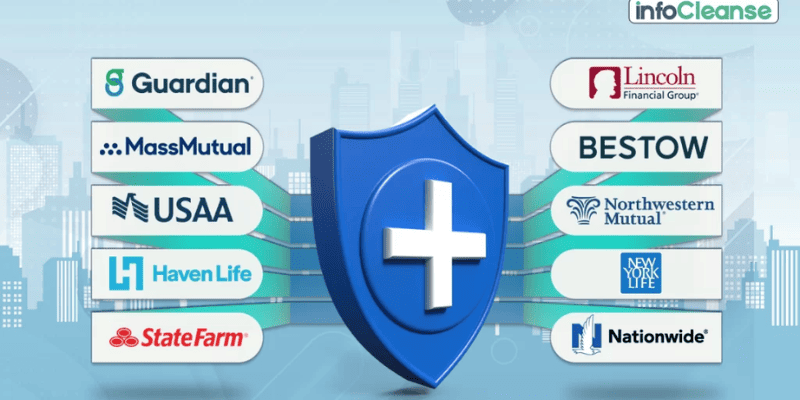

While Servicemembers’ Group Life Insurance (SGLI) and Veterans’ Group Life Insurance (VGLI) provide essential government-sponsored benefits, many military families seek additional private coverage. Several highly-rated private insurers understand the unique needs of service members and offer tailored products. DoctinOnline has identified companies renowned for their commitment to the military community, excellent financial strength, and specialized policy features.

One of the most recognized names is USAA, which specifically designs its products for active military members, veterans, and their families. USAA consistently earns high marks for financial stability, with an A++ (Superior) rating. Their term life policies often include military-specific perks such as expedited coverage before deployment, coverage during wartime, and a $25,000 severe injury payment for eligible military duties. USAA also offers the ability to add up to $100,000 in coverage after major life events and guarantees coverage after leaving the military.

Another strong contender for military families is Navy Mutual Aid Association, often partnered with Navy Federal Credit Union to provide life insurance options. Navy Mutual is known for policies specifically designed for active duty service members, often with no combat or war exclusions, and offers coverage up to $1,500,000. Their offerings include both term and whole life insurance plans, such as the Level II Plus Term Plan and the Flagship Whole Life Plan, which builds tax-deferred cash value.

Beyond these specialized providers, other reputable companies like Military Benefit Association (MBA) and Uniformed Services Benefit Association (USBA) also cater to military members and their families. MBA offers term life coverage up to $1,000,000 for active duty, veterans, retirees, and spouses, with no war clause and portability. USBA, founded in 1959 to address the lack of war clause-free policies, partners with New York Life Insurance Company to offer various plans without military exclusions. Prudential is also noted for offering a variety of policies for active military and veterans, including term and universal life coverage, with some options available without a medical exam and no exclusions for mental health conditions such as PTSD or TBI. When considering the best life insurance companies for military families, comparing the specific features and financial ratings of these providers is essential to find a policy that aligns with individual needs.

Understanding Different Life Insurance Policy Types

Navigating the various types of life insurance policies is crucial for military families seeking to build a robust financial safety net. Each policy type is designed to meet different needs, offering varying levels of coverage duration, cash value accumulation, and flexibility. DoctinOnline aims to demystify these options, helping you understand which might be the best life insurance companies for military families based on the product fit.

Term Life Insurance

Term life insurance provides coverage for a specific period, or “term,” typically ranging. This type of insurance is particularly well-suited for young families, those with outstanding mortgages, or individuals who need coverage for a defined period, such as until their children are grown or a significant debt is paid off. The main advantage is its cost-effectiveness, allowing for substantial coverage at a lower premium compared to permanent options. However, once the term expires, coverage ends unless it is renewed or converted, often at a higher premium.

Whole Life Insurance

Whole life insurance is a type of permanent life insurance that provides lifelong coverage, as long as premiums are paid. Unlike term life, it does not expire and offers a guaranteed death benefit whenever the policyholder passes away. A key feature of whole life insurance is its cash value component, which grows over time at a guaranteed rate. This cash value can be accessed by the policyholder through loans or withdrawals during their lifetime, offering a potential source of funds for emergencies or other financial needs. Premiums for whole life policies are typically fixed and remain level for the life of the policy. While generally more expensive than term life initially, whole life offers predictability and a guaranteed accumulation of cash value, making it suitable for long-term financial planning and estate considerations. The VA also offers Veterans Affairs Life Insurance (VALife), a whole life option for disabled veterans, providing guaranteed acceptance and fixed premiums for life, although with potentially lower coverage amounts.

Universal Life Insurance

Universal life insurance is another form of permanent life insurance, offering lifelong coverage with more flexibility than whole life policies. It also includes a cash value component that grows over time. The primary advantage of universal life is its adjustable premiums and death benefits. Policyholders may have the option to increase or decrease their coverage amount and vary their premium payments, within certain limits, depending on their financial situation and policy performance. This flexibility can be attractive to individuals whose financial needs or income streams may fluctuate over time. However, this flexibility also introduces a degree of complexity, as the cash value growth can be affected by market performance or changes in interest rates, and careful management is required to ensure the policy remains adequately funded.

Navigating Exclusions And Riders For Military Life

Understanding the fine print of an insurance contract, particularly concerning exclusions and available riders, is paramount for military families. These often-overlooked details can significantly impact a policy’s effectiveness during critical times. DoctinOnline emphasizes the importance of scrutinizing these sections to ensure comprehensive coverage.

Exclusion clauses specify circumstances under which the insurance company will not pay a death benefit. For military members, the most relevant are “war clauses” or military service clauses, which, as previously noted, might exclude coverage for deaths resulting. While Servicemembers’ Group Life Insurance (SGLI) and Veterans’ Group Life Insurance (VGLI) do not contain such exclusions, many private policies historically did, and some still might. It is critical to confirm that any private life insurance policy chosen for military families explicitly covers service-related deaths, deployments, and hazardous duties. Some companies specializing in military coverage, like USAA and Navy Mutual, are known for offering policies without these restrictive clauses.

Riders are optional additions to a life insurance policy that enhance or modify its coverage. For military families, certain riders can offer invaluable additional protection:

- Accelerated Death Benefit Rider: This rider allows policyholders to access a portion of their death benefit while still alive if diagnosed with a terminal illness. This can provide crucial financial relief during a difficult time.

- Waiver of Premium Rider: If the policyholder becomes totally disabled and unable to work, this rider waives future premium payments, keeping the policy in force. This is particularly relevant given the physical demands and potential for injury in military service.

- Child Life Insurance Rider: This provides a small amount of term life insurance coverage for eligible dependent children, often convertible to a permanent policy later, ensuring their future insurability.

- Guaranteed Insurability Rider: This allows the policyholder to purchase additional coverage at specified future dates or after certain life events (like marriage or the birth of a child) without needing another medical exam. This is especially useful for young military members whose insurance needs may grow over time.

Military Severe Injury Benefit Rider: Specific to military-friendly insurers like USAA, this rider provides a payment, such as $25,000, if the service member suffers certain severe injuries while performing eligible military duties.

- Carefully reviewing these exclusions and considering beneficial riders can significantly strengthen the financial protection offered by the best life insurance companies for military families.

The Claims Process And Company Financial Strength

When the unforeseen occurs, the efficiency and reliability of the claims process become paramount. For military families, understanding how to navigate this process and the importance of an insurer’s financial strength can alleviate significant stress during a time of loss. DoctinOnline stresses that a streamlined claims procedure and a financially robust company are non-negotiable aspects of a quality life insurance policy.

The claims process typically begins with notifying the insurance company of the policyholder’s death. Beneficiaries will generally need to complete a claim form and submit a certified copy of the death certificate. Some insurers, particularly those serving the military community like USAA and USBA, are known for their dedicated support teams and expedited processing, sometimes paying benefits within a few days of receiving all necessary documentation. For SGLI, the Casualty Assistance Office in the service member’s branch helps coordinate the claim, requiring specific forms and a certified death certificate.

However, claims can be delayed if paperwork is incomplete or if the death occurs within the first two years of the policy, prompting the insurer to investigate the cause of death. This highlights the importance of keeping policy documents organized and ensuring beneficiaries are aware of the policy and the claims procedure.

The insurer’s financial strength directly underpins its ability to pay claims promptly and reliably. Independent ratings agencies like AM Best provide crucial insights into a company’s fiscal health. For instance, an A++ (Superior) rating. Life insurance is a long-term commitment, and selecting a company with stellar financial ratings provides assurance that the promise of protection will be honored when it matters most. DoctinOnline consistently advises prioritizing insurers with superior financial strength to ensure your family’s financial security.

Final Thoughts

Choosing the best life insurance companies for military families is a critical decision that requires careful consideration of unique service-related factors and robust policy features. DoctinOnline hopes this comprehensive guide has illuminated the distinct needs, essential policy types, crucial exclusions, valuable riders, and the importance of financial strength in an insurer. By prioritizing companies that understand the military lifestyle, offer comprehensive coverage without restrictive war clauses, and demonstrate superior financial stability, you can secure the peace of mind that your loved ones will be financially protected, no matter what the future holds. We encourage you to review your current coverage, assess your family’s evolving needs, and consult with a trusted advisor to tailor a life insurance strategy that truly serves your family’s best interests.

{kind=link}