Homeownership is often considered a cornerstone of financial stability, but managing a mortgage efficiently is key to maximizing its benefits. For many, navigating the complexities of refinancing can seem daunting, especially with varying loan products and market conditions. In this article, DoctinOnline will accompany you to explore the FHA Streamline Refinance program, a specialized option for current FHA loan holders. We will delve into its unique characteristics, evaluate its advantages and potential drawbacks, and ultimately answer whether is FHA streamline refinance a good idea for your specific financial objectives. Understanding this program’s nuances is crucial for making informed decisions that align with your long-term wealth management strategy.

Understanding FHA Streamline Refinance

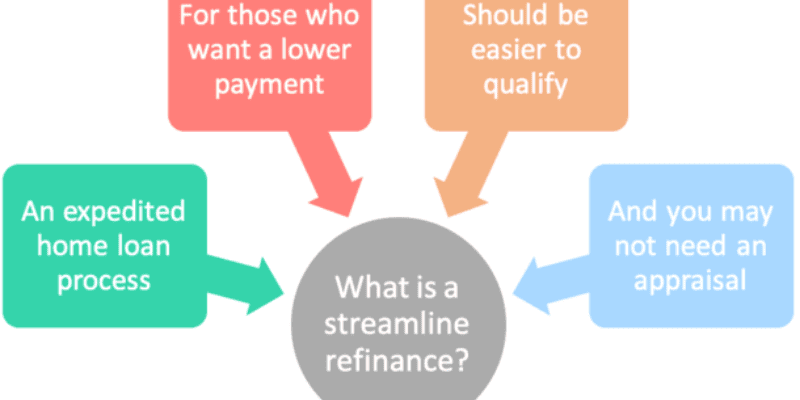

An FHA Streamline Refinance is a specific mortgage refinancing program designed for homeowners who currently possess an FHA-insured mortgage. The primary objective of this program is to simplify the refinancing process, making it quicker and less burdensome than traditional refinancing options. Its “streamlined” nature stems. The core purpose is to help borrowers achieve a “net tangible benefit,” typically a lower interest rate, reduced monthly payments, or a conversion from an adjustable-rate mortgage (ARM) to a more stable fixed-rate mortgage.

This program serves to enhance the affordability of the loan, thereby lowering the risk of default for borrowers, which ultimately benefits the Federal Housing Administration (FHA) as the insurer. Unlike conventional refinance products, the FHA Streamline is tailored exclusively for existing FHA loan holders and does not permit refinancing into other loan types. It offers a unique pathway for eligible individuals to improve their loan terms without undergoing the extensive verification processes typically associated with new mortgage applications.

Credit-Qualifying Versus Non-Credit Qualifying Options

The FHA Streamline Refinance program is broadly categorized into two main types: credit-qualifying and non-credit qualifying. These distinctions determine the level of financial scrutiny a borrower will undergo during the application process. The non-credit qualifying option is the most streamlined, as it often waives the need for a traditional credit check, income verification, or debt-to-income (DTI) ratio assessment. This can be particularly beneficial for borrowers whose financial circumstances may have changed since their original FHA loan, such as a decrease in income or a dip in credit score.

Conversely, a credit-qualifying FHA Streamline Refinance is typically required in situations where the refinance might lead to a significant increase in the mortgage payment, specifically by 20% or more, or if there is a removal of an original borrower. In these instances, lenders are mandated to verify income, assess creditworthiness, and review the DTI ratio to ensure the borrower can comfortably manage the new payment terms. While still simpler than a full refinance, the credit-qualifying route introduces more stringent checks to mitigate increased risk.

Unpacking the Benefits: Why Consider a Streamline Refinance

For eligible homeowners, the FHA Streamline Refinance program offers a compelling array of benefits designed to make their mortgage more manageable and affordable. The “streamlined” approach removes many of the common hurdles associated with traditional refinancing, providing a faster and often less costly path to improved loan terms. These advantages can translate into significant long-term savings and enhanced financial peace of mind.

One of the most appealing features is the ability to bypass a new home appraisal. This means the loan amount is determined by what is owed on the existing mortgage, not the home’s current market value. This is particularly advantageous for those with limited equity or whose homes may be “underwater,” meaning they owe more than the property is currently worth. Skipping the appraisal also removes an associated fee, contributing to lower upfront costs.

Furthermore, the reduced documentation requirements are a major draw. For non-credit qualifying streamlines, lenders often do not need to verify income, employment, or conduct a full credit check. This significantly accelerates the application process and makes refinancing accessible to borrowers who might otherwise struggle to meet stricter conventional lending criteria. The ability to secure a lower interest rate, which directly translates to reduced monthly payments, is a primary driver for many considering this option. This benefit can free up valuable cash flow for other financial goals or simply ease budget pressures.

The program also allows borrowers to convert an adjustable-rate mortgage (ARM) into a stable fixed-rate mortgage, providing predictability and protection against potential interest rate hikes. While mortgage insurance premiums (MIP) are still required, refinancing through a streamline could potentially lead to lower annual MIP rates, especially for older FHA loans. Additionally, some borrowers may even qualify for a partial refund of their upfront MIP paid on the original loan, which is applied as a discount on the new upfront MIP. These combined benefits underscore why for many, is FHA streamline refinance a good idea when looking to optimize their existing FHA mortgage.

Navigating Eligibility Requirements

While the FHA Streamline Refinance offers numerous advantages, it is not universally accessible. Specific criteria must be met to ensure eligibility for this specialized program. Understanding these requirements is the first step in determining whether this refinancing option aligns with your current financial standing and goals. The FHA designed these rules to ensure that the refinance provides a genuine benefit to the borrower and maintains the integrity of the FHA insurance program.

Must Have an Existing FHA Loan

The most fundamental requirement for an FHA Streamline Refinance is that you must already have an FHA-insured mortgage on the property you intend to refinance. This program is exclusively for FHA borrowers and cannot be used to refinance a conventional, VA, USDA, or any other type of loan. If you currently hold a different type of mortgage but wish to take advantage of FHA benefits, you would need to pursue a standard FHA refinancing loan, which involves a more comprehensive application process, including credit checks and income verification.

On-Time Payment History and Waiting Period

To qualify for an FHA Streamline Refinance, borrowers must demonstrate a responsible payment history on their existing FHA loan. Generally, you need to have made at least six on-time monthly payments, and a minimum of six months must have passed since your first payment due date. Additionally, at least 210 days must have elapsed since the closing date of your original FHA loan. While one 30-day late payment might be permitted within the last 12 months, all payments for the three months immediately preceding the refinance application must have been made on time. Maintaining a consistent payment record is crucial, as late payments can disqualify you.

Net Tangible Benefit Requirement

A cornerstone of the FHA Streamline Refinance program is the “net tangible benefit” rule. This FHA mandate ensures that the refinancing action genuinely improves the borrower’s financial situation. Simply put, the new loan must provide a clear and quantifiable advantage to the homeowner. This benefit can manifest in several ways: a reduction in the combined interest rate and mortgage insurance premium (MIP) by at least 0.5 percentage points; a conversion from an adjustable-rate mortgage (ARM) to a more stable fixed-rate mortgage; or a shortening of the loan term, which can lead to significant interest savings over the life of the loan. The FHA’s intention is to prevent borrowers.

The Cost Side: Closing Expenses and Mortgage Insurance

While an FHA Streamline Refinance is designed to be less costly and complicated than a traditional refinance, it is important for homeowners to understand that it is not entirely free. There are still associated expenses that must be factored into your financial planning. Being aware of these costs upfront allows for a more accurate assessment of the overall benefit and helps determine if is FHA streamline refinance a good idea for your individual circumstances.

Closing Costs

Despite the “streamline” nature, FHA Streamline Refinances do involve closing costs, similar to other mortgage transactions. These can include loan origination fees, title fees, and recording fees. While these costs are typically lower than those for a full conventional refinance, largely because an appraisal is usually not required, they can still range from 2% to 6% of the loan amount. A key difference. Borrowers must either pay these fees out-of-pocket, or some lenders may offer a “no-closing-cost” option where they cover the fees in exchange for a slightly higher interest rate. It is essential to obtain a detailed loan estimate.

Mortgage Insurance Premiums (MIP)

A significant aspect of FHA loans, including streamline refinances, is the requirement for mortgage insurance premiums (MIP). Unlike conventional loans where Private Mortgage Insurance (PMI) can eventually be removed once sufficient equity is built, FHA MIP typically remains for the life of the loan if the initial down payment was less than 10%. When undertaking an FHA Streamline Refinance, borrowers will be required to pay both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP), which is typically paid monthly as part of the mortgage payment. The current UFMIP is 1.75% of the loan amount, and annual MIP rates vary based on loan amount, loan-to-value (LTV) ratio, and loan term, generally ranging between 0.15% and 0.75%. While a partial refund of the original UFMIP may be applied if refinancing within three years, the ongoing cost of MIP is a crucial consideration when calculating the net savings of a streamline refinance.

Impact on Credit Score

The effect of an FHA Streamline Refinance on your credit score largely depends on whether you opt for a credit-qualifying or non-credit qualifying loan. For non-credit qualifying applications, the FHA itself does not require a credit check, meaning the impact on your credit score would be minimal to non-existent from the FHA’s perspective. However, some individual lenders may still choose to perform a soft credit pull even for non-credit qualifying loans, and any new mortgage will appear on your credit report. For a credit-qualifying FHA Streamline Refinance, a hard credit pull is typically performed, which can temporarily lower your credit score by a few points. Generally, the impact is considered less significant and shorter-lived compared to applying for an entirely new mortgage with extensive underwriting.

When Is FHA Streamline Refinance A Good Idea For You?

Deciding whether is FHA streamline refinance a good idea for your financial situation requires a careful evaluation of current market conditions, your personal financial health, and your long-term goals. While the program offers a simplified path to refinancing, it is most beneficial under specific circumstances. As a financial analyst, I emphasize a data-driven approach to this decision, ensuring that any move provides a genuine and sustainable benefit.

One of the most compelling reasons to consider an FHA Streamline Refinance is when interest rates have significantly dropped since you originated your existing FHA loan. Even a modest reduction in your interest rate can lead to substantial savings over the life of your mortgage, making your monthly payments more affordable. This direct reduction in borrowing costs is a clear net tangible benefit that the FHA program prioritizes.

Furthermore, if you currently have an adjustable-rate mortgage (ARM) and are concerned about future interest rate increases, converting to a fixed-rate mortgage through an FHA Streamline Refinance can provide invaluable payment stability. This switch eliminates the uncertainty of fluctuating payments, allowing for more predictable budgeting and long-term financial planning. The peace of mind that comes with a stable payment can be a significant advantage in volatile economic climates.

For borrowers whose credit scores have improved considerably since they first obtained their FHA loan, a credit-qualifying streamline refinance could unlock even better interest rates than initially available. While the non-credit qualifying option is available for those with less-than-perfect credit, leveraging an improved credit profile can lead to more favorable loan terms and greater savings. Additionally, if you have experienced a reduction in income and are finding it challenging to keep up with your current monthly payments, the FHA Streamline Refinance, particularly the non-credit qualifying variant, can offer much-needed relief by reducing your payments without requiring extensive income verification. This makes it an accessible option for maintaining homeownership during unexpected financial shifts. Finally, for those who simply seek a faster, easier refinancing process with less paperwork and quicker approval times, the streamlined nature of the FHA program presents an attractive solution.

Alternatives and Strategic Considerations

While an FHA Streamline Refinance presents a compelling option for many existing FHA loan holders, it is crucial to consider it within the broader landscape of refinancing strategies. A holistic financial approach involves examining all available alternatives to ensure the chosen path optimally serves your investment goals and long-term wealth accumulation. Sometimes, another refinancing product might align better with specific objectives, such as eliminating mortgage insurance or accessing home equity.

Conventional Refinance

For homeowners who have built substantial equity in their property, a conventional refinance might be a more suitable alternative to an FHA Streamline. A primary advantage of conventional loans is the ability to eliminate mortgage insurance (PMI) once you have at least 20% equity in your home. This can lead to significant monthly savings, potentially outweighing the benefits of lower interest rates alone, conventional refinances usually come with more stringent credit score and debt-to-income ratio requirements and will always require a new appraisal.

FHA Cash-Out Refinance

If your primary goal is to tap into your home equity for purposes such as home renovations, debt consolidation, or other significant expenses, an FHA Streamline Refinance is not the appropriate tool. Streamline programs typically limit cash-back to an incidental amount, usually not exceeding $500. In such cases, an FHA Cash-Out Refinance would be the more suitable option. This program allows you to refinance your existing FHA loan for a higher amount than you currently owe, providing you with a lump sum of cash. However, be aware that a cash-out refinance will involve a full appraisal, income and credit verification, and typically results in a higher loan amount, potentially increasing your overall interest payments and MIP.

Long-Term Financial Goals and Break-Even Point

Before committing to any refinance, it’s essential to analyze your long-term financial goals and calculate the break-even point. This is the amount of time it will take for the savings.

Final Thoughts

The FHA Streamline Refinance program offers a valuable opportunity for eligible homeowners to improve their mortgage terms, making their financial obligations more manageable and predictable. Whether is FHA streamline refinance a good idea for your particular situation hinges on a thorough understanding of its unique benefits, such as reduced documentation and the possibility of no appraisal, alongside careful consideration of the associated costs and eligibility criteria. By objectively assessing your current FHA loan, payment history, and financial goals, you can leverage this program to secure a lower interest rate, reduce monthly payments, or transition to a more stable fixed-rate mortgage. DoctinOnline encourages you to meticulously review your options, consult with trusted financial professionals, and make a decision based on data and disciplined analysis to foster your journey towards financial freedom.

{kind=link}