For many homeowners, the equity built in their property represents a significant, yet often untapped, financial asset. As a seasoned financial analyst, I consistently emphasize the importance of understanding all available tools for wealth management. In this article, DoctinOnline will accompany you to explore a powerful option for accessing this value: the fha cash out refinance max ltv. This specific refinancing strategy, backed by the Federal Housing Administration, allows you to convert a portion of your home’s equity into liquid cash, offering flexibility for various financial goals,, particularly the maximum loan-to-value (LTV) limits, is crucial for making an informed and responsible investment decision.

Understanding the FHA Cash Out Refinance

An FHA cash-out refinance is a mortgage refinancing option insured by the Federal Housing Administration that allows homeowners to leverage their accumulated home equity. Essentially, you replace your existing mortgage with a new, larger FHA-backed loan, receiving the difference between your old loan balance and the new one as a lump sum of cash. This program is not exclusive to existing FHA loan holders; borrowers with conventional mortgages or even those who own their homes outright can qualify, provided they meet specific FHA guidelines. The primary appeal lies in its more flexible eligibility criteria compared to conventional loans, making it accessible to a broader range of homeowners who might not possess perfect credit scores.

The core benefit of this refinancing strategy is its ability to unlock the wealth tied up in your home, transforming it into usable capital. Historically, home equity has been a solid, appreciating asset, but accessing it typically required selling the property. Refinancing, particularly through a cash-out option, provides a pathway to utilize this asset without relinquishing homeownership. However, like any financial instrument, it comes with specific parameters and costs that demand careful evaluation. Responsible investing means understanding both the opportunities and the obligations associated with such a significant financial move.

Deciphering the FHA Cash Out Refinance Max LTV

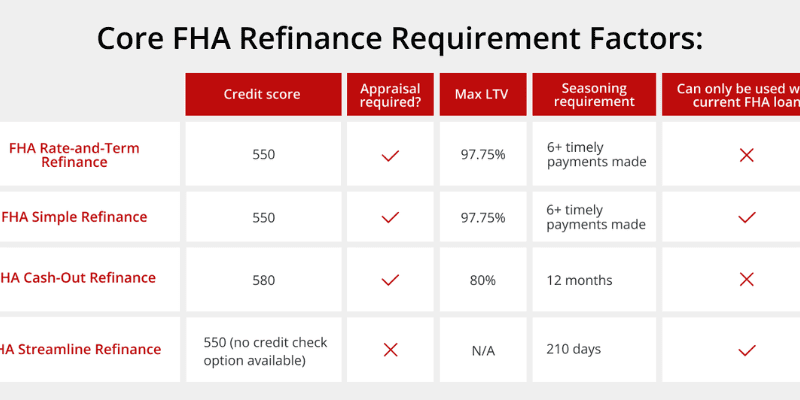

Central to understanding how much cash you can access from your home’s equity through this program is the concept of the Loan-to-Value (LTV) ratio. The LTV ratio is a critical metric calculated by dividing the loan amount by the appraised value of your home. For an fha cash out refinance max ltv, the Federal Housing Administration sets a strict limit to ensure borrowers retain a healthy portion of equity and to mitigate risk for lenders. Currently, the maximum LTV allowed for an FHA cash-out refinance is 80% of your home’s appraised value. This means your new, larger FHA mortgage, including the cash you receive, cannot exceed 80% of what your property is independently valued at.

To illustrate this, consider a home appraised at $400,000 where the current mortgage balance is $150,000. With an 80% LTV limit, the maximum new loan amount would be $320,000 ($400,000 x 0.80). After paying off the existing $150,000 mortgage, the homeowner could potentially receive $170,000 in cash before accounting for closing costs and other fees. This calculation underscores the importance of a professional home appraisal, as it directly determines your borrowing capacity. Moreover, it is vital to remember that the new mortgage must also fall within the FHA loan limits for your specific county, which can vary and may place an additional cap on the maximum amount available, especially in higher-value housing markets.

Key Eligibility Requirements for FHA Cash Out Refinance

While the fha cash out refinance max ltv offers a more lenient path to equity access than some conventional options, specific criteria must be met to qualify. As a financial advisor, I always stress the importance of reviewing these requirements well in advance to ensure a smooth application process and increase your chances of approval. Adherence to these guidelines demonstrates financial prudence and a commitment to responsible borrowing, principles that DoctinOnline consistently advocates.

Credit score considerations

Credit score requirements for FHA loans are generally more forgiving than those for conventional mortgages. The FHA technically allows for a minimum credit score as low as 500, though this often comes with more stringent conditions. Most lenders, acting with their own overlays, typically require a minimum FICO score of 580, and often prefer 600 to 620 or higher for an FHA cash-out refinance, recognizing the slightly increased risk associated with withdrawing equity. A stronger credit profile not only enhances your eligibility but can also lead to more favorable interest rates and terms on your new loan.

Debt-to-income ratios

Your debt-to-income (DTI) ratio is another crucial factor lenders assess, measuring your monthly debt payments against your gross monthly income. The FHA typically looks for a DTI ratio of 43% or less. However, there can be some flexibility; with a higher credit score (e.g., 580 or above) and significant compensating factors, such as ample cash reserves, borrowers might be approved with a DTI up to 50% or even 56.9% in certain scenarios. This flexibility is one of the distinguishing characteristics of FHA loans, providing opportunities for those with manageable, though not minimal, debt loads.

Occupancy and payment history

To qualify for an FHA cash-out refinance, the property must be your primary residence, and you must have occupied it for at least the 12 months preceding your application. This requirement underscores the FHA’s mission to support homeownership for primary residents, not investment properties. Furthermore, a consistent and timely mortgage payment history is paramount. You are generally required to have made all mortgage payments on time for the past 12 months, or since the origination of your current loan if it’s less than a year old. Demonstrating financial discipline through a solid payment record is a non-negotiable element for securing this type of refinance.

The Costs and Considerations of an FHA Cash Out Refinance

While an FHA cash-out refinance can be an attractive option for accessing home equity, it’s crucial to understand the associated costs and long-term implications. As responsible investors, we must always weigh the benefits against the expenses to determine the true financial viability of any strategy. DoctinOnline emphasizes transparency in financial planning, so let’s delve into what you can expect.

Closing costs and upfront MIP

Like all mortgage transactions, an FHA cash-out refinance involves closing costs. These typically range from 2% to 6% of the total loan amount and cover various fees such as appraisal fees, origination fees, title insurance, and government taxes. In addition to these standard costs, FHA loans require an Upfront Mortgage Insurance Premium (UFMIP). This is a one-time fee of 1.75% of the new loan amount, which can either be paid at closing or rolled into your mortgage, increasing your loan balance. While rolling it in can reduce your immediate out-of-pocket expenses, it means you’ll pay interest on this premium over the life of the loan.

Annual mortgage insurance premium (MIP)

Beyond the UFMIP, all FHA loans, including cash-out refinances, require an Annual Mortgage Insurance Premium (MIP). This premium is paid monthly and is calculated as a percentage of the loan amount, typically around 0.55% as of recent guidelines, though it can range.45% to 0.80% depending on the loan-to-value ratio and term. A significant distinction from conventional loans is that FHA’s annual MIP generally lasts for the entire life of the loan, regardless of how much equity you build. This ongoing cost can significantly impact the overall expense of your loan, particularly when comparing it to a conventional cash-out refinance where private mortgage insurance (PMI) can often be removed once you reach 20% equity.

Increased debt and monthly payments

Opting for a cash-out refinance inherently means taking on a larger mortgage, as you’re borrowing more than your current outstanding balance. This increased debt load will almost certainly lead to higher monthly mortgage payments, even if you secure a favorable interest rate. Before proceeding with an fha cash out refinance max ltv, it is imperative to conduct a thorough financial analysis to ensure that your new, higher monthly obligations are comfortably sustainable within your budget. Failing to do so could strain your finances and undermine your long-term wealth accumulation goals, directly contradicting the principles of sound financial discipline.

Strategic Uses for Your Cash Out Funds

One of the most compelling aspects of an FHA cash-out refinance is the flexibility it offers in how you utilize the retrieved funds. Unlike some other lending products with restricted purposes, the cash obtained, I advise strategic deployment of these funds to maximize long-term financial benefit rather than simply funding discretionary spending.

Home improvements and value enhancement

A highly recommended use of cash-out funds is for home improvements or renovations that enhance your property’s value. Investing in a new kitchen, bathroom remodel, or adding functional living space can often yield a strong return on investment when it comes time to sell. This approach effectively recycles your home’s equity back into the asset, potentially increasing its appraisal value and strengthening your overall net worth. Smart renovations are not just about aesthetics; they are about strategic asset management that aligns with your financial goals.

Debt consolidation

Another common and often beneficial application of cash-out proceeds is debt consolidation. By paying off higher-interest debts, such as credit card balances or personal loans, you can streamline your monthly payments into a single, potentially lower-interest mortgage payment. FHA cash-out refinance rates are generally more competitive than rates on unsecured debts, making this a prudent move for reducing interest expenses and accelerating your path to becoming debt-free. This strategy demands discipline to avoid accumulating new high-interest debt after consolidating.

Investment opportunities or emergency funds

For those with a solid financial foundation and a clear understanding of risk, cash-out funds can be strategically allocated to investment opportunities or bolster an emergency fund. Investing in a diversified portfolio, contributing to a retirement account, or even starting a small business could potentially generate returns that outweigh the cost of the mortgage. Alternatively, building a robust emergency fund provides a crucial financial safety net, protecting your assets and maintaining peace of mind during unexpected life events. This approach aligns with DoctinOnline’s philosophy of data-driven investment and disciplined financial planning.

Exploring Alternatives to an FHA Cash Out Refinance

While an FHA cash-out refinance can be a valuable tool, it is essential to consider all available options to determine the best fit for your unique financial situation. As an experienced financial professional, I always advocate for a comprehensive analysis of alternatives. Each option carries its own set of advantages and disadvantages, particularly when compared to the fha cash out refinance max ltv and its inherent mortgage insurance requirements.

Conventional cash out refinance

For homeowners with strong credit scores (typically 620 or higher) and substantial equity, a conventional cash-out refinance often presents a more cost-effective alternative. The primary advantage of a conventional cash-out loan at 80% LTV or less is the absence of mandatory private mortgage insurance (PMI). This can lead to significant long-term savings compared to an FHA loan, where the annual MIP typically remains for the life of the loan, regardless of equity buildup. Conventional loans also offer more flexibility for refinancing second homes or investment properties, which FHA loans do not permit.

Home equity loans (HELs) and HELOCs

If you prefer not to replace your entire first mortgage but still want to access your home equity, a Home Equity Loan (HEL) or a Home Equity Line of Credit (HELOC) can be viable options. A HEL is a second mortgage that provides a lump sum of cash with a fixed interest rate, repayable over a set term. A HELOC, conversely, functions like a revolving credit line, allowing you to borrow funds as needed up to a certain limit during a draw period, with interest only on the amount borrowed. Both options allow you to keep your existing first mortgage, which can be advantageous if you have a very low interest rate on your current loan. However, they introduce a second lien on your property and typically come with variable interest rates for HELOCs or higher fixed rates for HELs compared to a primary mortgage.

FHA streamline refinance

For existing FHA loan holders primarily seeking to lower their interest rate or change their loan term without needing significant cash, an FHA Streamline Refinance could be ideal. This program offers a simplified application process with less paperwork and often no appraisal or credit underwriting requirement. However, the cash-out component is extremely limited, usually capped at around $500, making it unsuitable for those looking to tap into substantial home equity. It serves a different purpose than the fha cash out refinance max ltv, focusing on making current FHA mortgages more affordable or manageable for the homeowner.

Conclusion

The fha cash out refinance max ltv stands as a powerful tool for homeowners seeking to unlock the equity built in their primary residence, offering a clear pathway to liquidity for various financial objectives. Understanding the 80% maximum loan-to-value ratio, alongside the specific credit, DTI, occupancy, and payment history requirements, is fundamental to making an informed decision. While this option provides greater flexibility in qualification, it is critical to account for the upfront and annual mortgage insurance premiums, which represent a significant ongoing cost. Before committing, DoctinOnline urges you to meticulously assess these costs against the benefits, ensuring the refinance aligns with your long-term financial goals and does not lead to an unsustainable increase in your debt burden. Explore all alternatives and consult with a qualified financial professional to determine if this strategy is the most responsible choice for your unique investment portfolio and wealth management plan.

{kind=link}