Navigating the complexities of homeownership involves making strategic financial decisions that can significantly impact your long-term wealth. One such powerful tool in a homeowner’s arsenal is mortgage refinancing. In a dynamic economic landscape characterized by fluctuating interest rates and evolving market conditions, understanding when can you refinance a house effectively becomes paramount for optimizing your financial health. Today, let’s join DoctinOnline to find out how to strategically approach this decision, ensuring that any move you make is well-informed, data-driven, and aligned with your broader financial objectives. This analysis will delve into the critical factors that determine the opportune moments for refinancing, empowering you to make choices that enhance your financial freedom and prepare for a secure future.

Understanding Mortgage Refinancing: What It Is And Why It Matters

Mortgage refinancing involves replacing your existing home loan with a new one, typically to secure more favorable terms or to tap into your home’s equity. This financial maneuver is more than just securing a lower interest rate; it is a strategic decision that can reshape your monthly budget, reduce the overall cost of your loan, or even provide liquidity for other investments or needs. Historically, homeowners have utilized refinancing to adapt their mortgage to changing personal financial situations or shifts in the broader economic environment, turning what might seem like a complex process into a clear pathway for significant savings and financial flexibility. It demands a thorough understanding of current market conditions, your personal financial standing, and the potential implications for your long-term investment strategy.

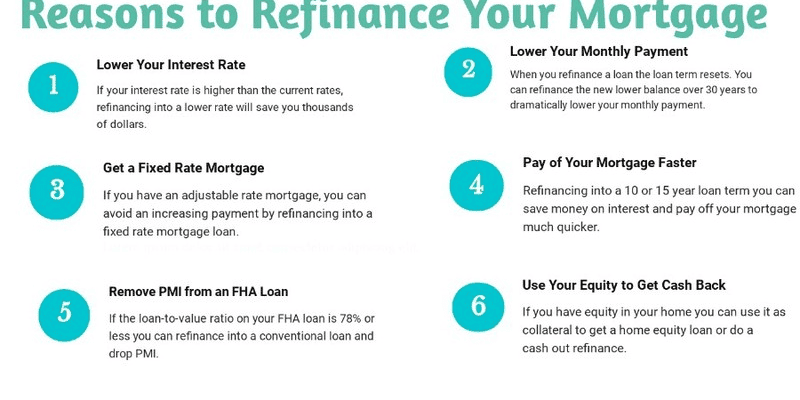

The primary motivations for homeowners to consider refinancing are diverse, ranging, can drastically reduce the total interest paid and accelerate your path to mortgage-free homeownership. For those looking to consolidate higher-interest debt or fund significant life events, a cash-out refinance allows homeowners to convert a portion of their home equity into liquid funds. Each of these scenarios presents a unique set of benefits and considerations, necessitating careful evaluation against your personal financial goals and risk tolerance.

Key Financial Indicators Dictating Refinancing Opportunities

Determining when can you refinance a house profitably requires a keen eye on several pivotal financial indicators. These metrics, when analyzed collectively, paint a comprehensive picture of whether the current environment and your personal circumstances align for a beneficial refinancing decision. Ignoring any of these factors could lead to a less-than-optimal outcome, potentially costing you more in the long run rather than achieving the desired savings. Savvy investors understand that timing is critical in finance, and refinancing is no exception.

Interest Rate Movements

The most significant driver for refinancing decisions is often a notable drop in prevailing interest rates. When market rates fall below your current mortgage rate, the opportunity to secure a lower rate and consequently a reduced monthly payment becomes compelling. This often occurs in response to broader economic shifts, such as changes in the Federal Reserve’s monetary policy or reactions to economic slowdowns designed to stimulate lending and growth. For instance, a drop of even half a percentage point can translate into thousands of dollars saved over the life of a substantial loan. Financial analysts frequently monitor the yield on the 10-year Treasury note, as it often serves as a benchmark for long-term mortgage rates, providing an early indication of potential rate changes. Keeping a close watch on these trends is essential for identifying a window of opportunity.

Improving Credit Scores

Your credit score plays a critical role in determining the interest rate you qualify for on a new mortgage. A significant improvement in your credit score since you originally obtained your mortgage can open doors to much better terms during a refinance, even if market rates haven’t changed dramatically. Lenders view borrowers with higher credit scores as less risky, offering them more competitive rates and favorable conditions. This improvement could be due to consistent on-time payments across all your debts, a reduction in your overall debt load, or a longer credit history. Before considering a refinance, assessing your current credit standing and taking steps to enhance it if necessary can yield substantial benefits in the form of a lower interest rate and reduced closing costs.

Increased Home Equity

An increase in your home equity, whether through consistent principal payments or appreciation in your home’s market value, can also present an opportune moment to refinance. Greater equity provides a larger buffer for lenders, potentially qualifying you for a lower loan-to-value (LTV) ratio, which can result in better interest rates and even the elimination of private mortgage insurance (PMI) if your LTV drops below 80%. Moreover, a substantial increase in equity is what makes cash-out refinancing a viable option for those looking to access funds for home improvements, education, or debt consolidation. Understanding your current equity position is therefore a crucial step in evaluating the potential benefits and eligibility for various refinancing products.

Debt Consolidation And Cash-Out Refinancing

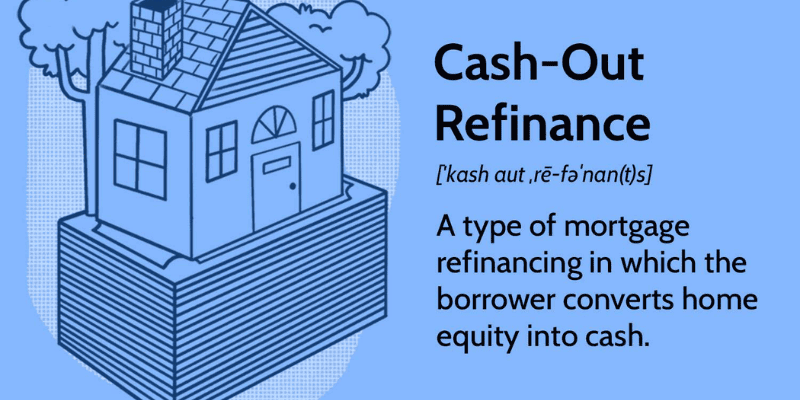

Beyond simply securing a lower interest rate, refinancing offers a powerful mechanism for strategic debt management. A cash-out refinance, specifically, allows homeowners to borrow against their accumulated home equity, converting a portion of that equity into liquid funds. This can be particularly advantageous for consolidating high-interest debts, such as credit card balances or personal loans, into a single, lower-interest mortgage payment. While this strategy can significantly reduce monthly outgoings and the overall interest paid on those debts, it is critical to use the funds wisely and avoid simply re-accumulating new high-interest debt. The decision to pursue a cash-out refinance should align with a clear financial plan, demonstrating financial discipline and a thorough understanding of the long-term implications of extending mortgage debt.

Calculating The Right Moment To Refinance Your Mortgage

Pinpointing the exact moment to initiate a refinance goes beyond merely observing favorable market conditions; it involves a rigorous personal financial analysis. Making an informed decision about when can you refinance a house optimally requires a strategic calculation of the costs involved against the potential savings. This careful consideration ensures that the financial benefits outweigh the upfront expenses, leading to genuine long-term value. Without this analytical approach, even a seemingly attractive interest rate might not translate into real financial advantage.

One of the most crucial calculations is the break-even analysis. This involves determining how long it will take for the savings, if your closing costs are $3,000 and your new mortgage saves you $100, your break-even point would be 30 months (3,000 / 100 = 30). If you plan to sell your home or refinance again before reaching that break-even point, the refinance might not be financially beneficial. This analysis is critical because it forces you to consider your future housing plans in conjunction with the immediate financial impact of refinancing.

Another significant consideration is the remaining term of your current loan. If you are already several years into a 30-year mortgage, refinancing into a new 30-year loan, even with a lower interest rate, could restart your amortization schedule and ultimately lead to paying more interest over a longer period. While your monthly payments might decrease, the extended term means you’re prolonging your debt obligation. A better strategy might be to refinance into a shorter-term loan, such as a 15-year mortgage, if your budget allows for higher monthly payments. This approach accelerates your equity build-up and significantly reduces the total interest paid, aligning with the goal of achieving financial freedom sooner.

Navigating The Refinancing Process And Associated Costs

Embarking on a mortgage refinance journey requires a clear understanding of the process and, importantly, the associated costs. While the prospect of securing better terms is enticing, these upfront expenses can sometimes dilute the immediate benefits. Approaching this phase with transparency and meticulous planning is key to ensuring that the refinancing decision genuinely contributes to your long-term financial prosperity. Understanding these elements beforehand helps manage expectations and facilitates a smoother transition to your new loan.

The refinancing process typically begins with gathering financial documents, including income verification, tax returns, and current mortgage statements, similar to your original home loan application. Lenders will then evaluate your creditworthiness, income, and debt-to-income ratio to determine your eligibility and the rates you qualify for. An appraisal of your home’s current market value is almost always required to confirm the property’s value and establish the loan-to-value ratio. This step is crucial, as a lower-than-expected appraisal could impact the terms offered or even your eligibility for certain refinance products. Diligent preparation of your documents and a proactive approach to any lender requests can significantly streamline this process, minimizing delays and potential frustrations.

The costs associated with refinancing, often referred to as closing costs, can range from 2% to 5% of the loan amount. These expenses are not negligible and include various fees such as application fees, loan origination fees, appraisal fees, title insurance, attorney fees, and recording fees. Some lenders offer “no-closing-cost” refinances, but this typically means the costs are rolled into the loan amount or compensated by a slightly higher interest rate, effectively still paying for them over time. It is imperative to obtain a detailed breakdown of all closing costs, as part of your break-even analysis, is fundamental to determining the true financial advantage of refinancing.

Strategic Advantages And Potential Pitfalls To Consider

Refinancing, when executed thoughtfully, can be a cornerstone of a sound financial strategy, offering distinct advantages that extend beyond mere interest rate reductions. However, like any significant financial decision, it comes with its own set of potential pitfalls that astute investors must recognize and mitigate. Understanding both the upsides and downsides is crucial for a balanced perspective on when can you refinance a house effectively. This comprehensive view ensures that your actions are driven by prudence and a clear understanding of the complete financial picture.

Lowering Monthly Payments

One of the most immediate and appealing benefits of refinancing is the potential to significantly lower your monthly mortgage payments. This is often achieved by securing a lower interest rate or by extending the loan term. A reduced monthly obligation can free up valuable cash flow, which can then be allocated to other critical financial goals. This could include increasing contributions to retirement accounts, building an emergency fund, investing in a diversified portfolio, or paying down other higher-interest debts more aggressively. For individuals and families seeking to improve their financial flexibility and reduce household expenses, a lower mortgage payment can be a powerful catalyst for achieving broader economic stability and long-term wealth accumulation.

Shortening Your Loan Term

Conversely, some homeowners choose to refinance into a shorter-term mortgage, such as moving from a 30-year to a 15-year loan. While this typically results in higher monthly payments, the long-term savings in interest can be substantial, and it accelerates the path to outright homeownership. This strategy is particularly attractive to those with stable or increasing incomes who are comfortable with a larger monthly commitment in exchange for significant future financial freedom. By reducing the total interest paid over the life of the loan, a shorter term refinance aligns with principles of sound financial management, allowing you to reallocate resources to other wealth-building endeavors much sooner.

The Risk Of Extending Your Debt Horizon

A significant pitfall, often overlooked, is the risk of extending your overall debt horizon. When refinancing a loan that is already several years old into a new 30-year term, you effectively reset the clock on your mortgage payments. Even if you secure a lower interest rate, you could end up paying more interest over the new, longer life of the loan than you would have on your original mortgage’s remaining term. This occurs because the initial years of a mortgage are heavily weighted towards interest payments. Therefore, while monthly payments may decrease, the total financial outlay might increase. This decision requires a careful comparison of the remaining interest on your current loan versus the total interest on the proposed new loan.

Impact On Overall Financial Planning

Refinancing decisions must be viewed within the context of your overall financial plan. A cash-out refinance, for instance, while providing immediate liquidity, increases your mortgage debt and potentially reduces the equity you’ve built. While seemingly beneficial for consolidating high-interest debt, it converts unsecured debt into secured debt against your home, putting your primary asset at greater risk if you face financial hardship. Similarly, frequent refinancing can lead to accumulating significant closing costs over time, eroding the benefits of rate reductions. Therefore, before committing to a refinance, consider how it aligns with your investment strategies, retirement goals, and risk tolerance, ensuring it contributes positively to your long-term wealth management rather than detracting.

Market Dynamics And Macroeconomic Influences

Understanding when can you refinance a house profitably is inextricably linked to comprehending broader market dynamics and macroeconomic forces. The decisions made by central banks, shifts in inflation, and the overall economic outlook have a profound impact on interest rates and the housing market, directly influencing the attractiveness and feasibility of refinancing. A seasoned financial analyst always keeps these larger trends in perspective, recognizing their potential to create both opportunities and challenges for homeowners.

The Federal Reserve’s monetary policy, particularly its decisions regarding the federal funds rate, serves as a powerful lever in the financial markets. While the federal funds rate is an overnight lending rate between banks, its adjustments cascade through the economy, influencing everything. Monitoring the Fed’s announcements and understanding their implications for future rate movements is crucial for anticipating opportune refinancing windows.

Inflation also plays a significant role in shaping interest rate environments. When inflation is high and persistent, lenders demand higher interest rates to compensate for the eroding purchasing power of future repayment dollars. This protective measure ensures that the real return on their loans remains positive. Therefore, periods of rising inflation often coincide with increasing mortgage rates, making refinancing less attractive. Conversely, during periods of low inflation or deflationary concerns, interest rates tend to fall, creating a more favorable climate for homeowners looking to secure lower rates. Analyzing inflation reports, such as the Consumer Price Index (CPI), provides critical insights into these underlying economic pressures and their potential impact on mortgage rates.

Furthermore, the overall economic outlook and the health of the housing market itself significantly influence refinancing conditions. A robust economy with strong job growth and consumer confidence often supports a stable or appreciating housing market, increasing home equity and making cash-out refinances more viable. Conversely, an economic downturn, coupled with job losses and a softening housing market, can lead to stagnant home values or even depreciation, limiting equity and making refinancing more challenging. Experts like Warren Buffett often emphasize the importance of understanding long-term economic cycles, advising against making impulsive financial decisions based solely on short-term market fluctuations. Ray Dalio of Bridgewater Associates similarly highlights the significance of “the big picture” macroeconomic trends. By considering these broader economic forces, homeowners can adopt a more strategic and disciplined approach to their refinancing decisions, aligning with the principles of long-term investment success championed by leading financial minds.

Conclusion

Understanding when can you refinance a house is a critical component of effective personal financial management, offering significant opportunities for optimizing your household budget and accelerating wealth accumulation. DoctinOnline hopes this in-depth analysis has provided you with a clear framework for evaluating the opportune moments, considering factors. By diligently analyzing your personal financial situation against market conditions and carefully calculating the break-even point of a refinance, you can make informed decisions that align with your long-term financial goals. We encourage you to consult with a qualified financial advisor to discuss your specific circumstances and explore how refinancing can contribute to building a sustainable investment portfolio and achieving your financial freedom.

{kind=link}