Welcome, car enthusiasts, to another in-depth analysis, where we cut through the marketing hype to deliver objective data and real-world insights. Today, we’re tackling a topic often overlooked in the excitement of a new car purchase, yet one that significantly impacts your total cost of ownership: insurance premiums. Understanding what cars have the cheapest insurance is paramount for any discerning buyer looking to make a financially sound decision. This isn’t just about the initial sticker price; it’s about the ongoing expenses that shape your long-term budget. In this article, DoctinOnline will delve into the engineering and market factors that dictate insurance rates, examine specific vehicle types and models known for lower premiums, and offer expert advice to help you minimize your annual outgoings without compromising on quality or safety.

Understanding insurance costs

Automobile insurance premiums are not arbitrary figures; they are meticulously calculated based on a complex algorithm of risk assessment. Insurers evaluate numerous variables to predict the likelihood and potential cost of a claim involving your vehicle. This intricate process involves analyzing data points ranging from the car’s inherent design and safety features to its repair costs, theft rates, and overall reliability statistics. Understanding these underlying factors is the first step in identifying what cars have the cheapest insurance and making an informed purchase decision. It moves beyond simply looking at a car’s aesthetic appeal or performance figures, focusing instead on its pragmatic financial implications over its lifespan.

Factors influencing premiums

Several critical factors contribute to the calculation of your car insurance premiums. The vehicle’s make, model, and year are fundamental, as these define its crashworthiness, repair complexity, and market value. For instance, cars with readily available parts and simpler repair processes typically incur lower costs after an accident, translating into more favorable insurance rates. The car’s safety features, such as advanced driver-assistance systems like automatic emergency braking or lane-keeping assist, can significantly reduce the risk of collisions, potentially leading to discounts. However, the sophistication of these systems can also mean higher repair costs if they are damaged, creating a delicate balance that insurers weigh carefully. The vehicle’s engine size and performance capabilities also play a role; high-horsepower sports cars, for example, are often associated with higher-risk driving behaviors and consequently higher premiums. Furthermore, the likelihood of theft for a particular model is factored in, with popular targets for thieves often commanding higher comprehensive coverage costs.

How insurers assess risk

Insurance companies employ vast databases and statistical models to assess the risk associated with each vehicle. They look at historical data on accident frequency and severity for specific models, the average cost of repairs for common types of damage, and the vehicle’s vulnerability to theft. A car that consistently performs well in crash tests, earning top safety ratings. The cost of parts and labor for specific models also influences risk assessment; vehicles with expensive, proprietary components or specialized repair procedures will naturally incur higher repair costs, which are reflected in higher premiums. This detailed evaluation ensures that the premium accurately reflects the potential financial exposure for the insurer, helping you understand what cars have the cheapest insurance from a data-driven perspective.

Vehicle characteristics that reduce insurance rates

When considering what cars have the cheapest insurance, certain inherent characteristics of a vehicle stand out as consistent indicators of lower premiums. These attributes are often tied directly to engineering principles focused on safety, durability, and cost-effectiveness of repair. Vehicles designed with these considerations in mind inherently present a lower risk profile to insurers, as they are less likely to be involved in severe accidents, are more resistant to theft, and are more affordable to fix when damage does occur. This makes them attractive not only to cost-conscious buyers but also to insurance providers who seek to minimize their payouts. Understanding these characteristics can guide your selection process, ensuring your next vehicle is not only a joy to drive but also economical to insure.

Safety features and ratings

Modern vehicles are equipped with an array of safety features designed to prevent accidents or mitigate their severity. Features such as multiple airbags, anti-lock brakes (ABS), electronic stability control (ESC), and advanced driver-assistance systems like blind-spot monitoring, forward collision warning, and lane departure warning, all contribute to a vehicle’s overall safety rating. Cars that consistently achieve top ratings from independent testing bodies like the Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) are often rewarded with lower insurance premiums. For example, a “Good” rating in IIHS crash tests or a 5-star NHTSA overall safety rating signifies superior occupant protection and crash avoidance capabilities, directly reducing the statistical likelihood of expensive injury claims. Insurers recognize that these technologies actively reduce risk, making vehicles equipped with them a more favorable proposition.

Reliability and repair costs

A vehicle’s reliability record and the associated costs of repair are major determinants of insurance premiums. Cars with a strong track record of reliability, often highlighted in J.D. Power and Consumer Reports surveys, experience fewer mechanical breakdowns and thus fewer potential claims related to component failures. Beyond mere breakdowns, the design and accessibility of components significantly influence repair costs after a collision. Vehicles engineered with modular components that are easy to replace, or those that utilize widely available and inexpensive parts, will generally cost less to repair than vehicles with complex, integrated systems or proprietary, high-cost components. For example, a minor fender bender in a car with simple bum. These factors directly impact the insurer’s potential payout for property damage claims, influencing what cars have the cheapest insurance.

Theft rates

The vulnerability of a vehicle to theft is another significant factor in determining comprehensive insurance premiums. Cars that are frequently targeted by thieves, or those that are easier to steal, will naturally have higher comprehensive coverage costs. Manufacturers often incorporate various anti-theft measures, such as immobilizers, alarm systems, and vehicle tracking devices, to deter theft. The effectiveness of these systems, combined with the overall popularity of a model among car thieves, is closely monitored by insurers. Vehicles with low theft rates are considered less risky assets, leading to more attractive insurance quotations. This consideration goes beyond just the physical security of the car; it also encompasses its market desirability to criminals, which can sometimes be influenced by the availability of its parts on the black market.

Top vehicle categories with affordable insurance

When exploring what cars have the cheapest insurance, it becomes clear that certain vehicle categories consistently offer more favorable rates than others. This is largely due to a combination of their inherent characteristics, typical driver demographics, and perceived risk profiles by insurance companies. Generally, vehicles that are practical, family-oriented, and less performance-focused tend to be more affordable to insure. These categories often emphasize safety, fuel efficiency, and lower repair costs, all of which are attractive attributes for insurers. Understanding these trends can help narrow down your search for a new vehicle, guiding you towards options that align with both your lifestyle needs and your budget for ongoing ownership costs.

Sedans and compact cars

Sedans and compact cars frequently rank among the most affordable vehicles to insure. Their smaller engine sizes generally imply lower performance capabilities, which insurers often associate with a reduced likelihood of high-speed accidents or reckless driving. Furthermore, these vehicles are typically mass-produced, leading to a readily available and relatively inexpensive supply of parts, which keeps repair costs down. Many sedans and compacts also boast strong safety ratings due to advanced engineering and standard safety features, making them a lower risk in the eyes of insurance providers. They are often purchased by individuals or families looking for reliable, economical transportation, which aligns with a lower-risk driver profile. The ubiquitous nature of sedans and compacts on our roads also means that repair shops are well-versed in their maintenance and repair, contributing to efficiency and cost savings.

Small SUVs and crossovers

While larger SUVs can be more expensive to insure due to their higher purchase price and potentially greater damage in a collision, small SUVs and crossovers often strike a balance between utility and affordability. These vehicles offer the versatility and higher driving position many buyers desire without the excessive weight or power of their larger counterparts. Many compact crossovers share platforms with sedans, which can translate to similar repair costs and parts availability. Their popularity has also driven manufacturers to equip them with a comprehensive suite of safety features to appeal to family buyers, further reducing their risk profile. Insurers view these vehicles as practical, family-friendly options, typically driven cautiously, which contributes to their more favorable insurance rates. The combination of practicality, safety, and manageable repair costs makes many small SUVs and crossovers a smart choice for those seeking what cars have the cheapest insurance.

Minivans

Minivans are almost universally recognized for their family-friendly design and utility, and they also tend to be among the least expensive vehicles to insure. Their primary purpose is to safely transport multiple passengers, meaning they are engineered with an emphasis on safety, stability, and practicality rather than high performance. Minivan drivers are typically perceived as responsible and cautious, aligning with a low-risk demographic for insurers. Their lower center of gravity compared to many SUVs contributes to better stability, while extensive safety features, including numerous airbags and robust child seat anchors, reduce the likelihood and severity of injuries in the event of an accident. Repair costs for minivans are often reasonable due to their commonality and straightforward construction, making them an excellent option for those prioritizing low insurance premiums alongside spaciousness and family functionality.

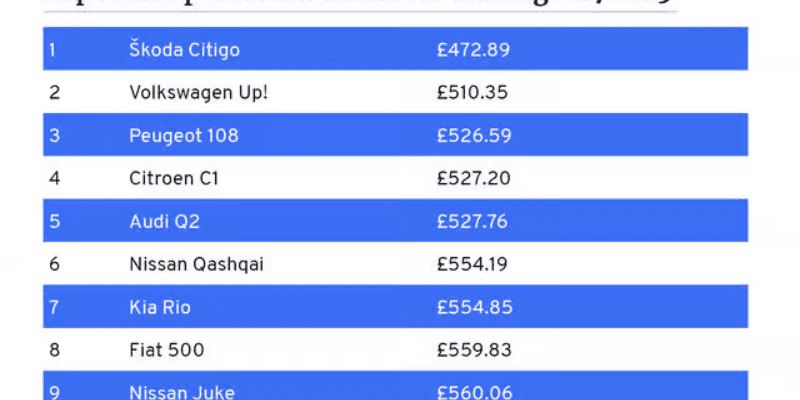

Specific models known for low insurance premiums

Identifying what cars have the cheapest insurance often boils down to examining specific models that consistently appear on “cheapest to insure” lists. These vehicles typically embody the characteristics discussed earlier: excellent safety ratings, high reliability, reasonable repair costs, and lower theft rates. While insurance premiums can vary based on individual factors such as driver history, location, and chosen coverage, these models generally offer a strong starting point for finding affordable rates. DoctinOnline emphasizes that market availability and regional specifics might slightly alter this, but the underlying engineering and market appeal of these vehicles generally lead to competitive insurance costs across the board.

Honda Civic

The Honda Civic is a perennial favorite for its reliability, fuel efficiency, and strong safety record, making it a consistent contender for low insurance premiums. Its widespread popularity ensures parts are readily available and affordable, contributing to lower repair costs. Honda’s commitment to safety engineering, with features like Honda Sensing, helps the Civic achieve excellent crash test ratings, which is a major factor for insurers. The Civic’s diverse trim levels,, but even the performance-oriented models often maintain reasonable insurance rates compared to dedicated sports cars. Its reputation for longevity also means fewer unexpected mechanical issues, further reducing the likelihood of certain claims.

Toyota Corolla

Much like the Civic, the Toyota Corolla is renowned globally for its unwavering reliability and robust engineering, which directly translates to lower insurance costs. Toyota’s reputation for building durable vehicles with simple, effective designs means fewer repairs and lower expenses when they are needed. The Corolla consistently earns high marks in safety tests, equipped with Toyota Safety Sense, a suite of advanced safety features that actively prevent collisions. Its modest horsepower and practical orientation mean it’s rarely associated with high-risk driving. The immense volume of Corollas produced and sold also contributes to easily accessible and affordable parts, making repairs straightforward and less costly for insurers. The Corolla is an exemplary answer to what cars have the cheapest insurance for many drivers.

Subaru Forester

The Subaru Forester, a compact SUV, consistently achieves high safety ratings due to Subaru’s Symmetrical All-Wheel Drive system, which enhances stability, and the EyeSight Driver Assist Technology. These features actively reduce the risk of accidents. While an SUV, its relatively conservative engine options and family-oriented design mean it doesn’t fall into the high-risk performance category. Subaru vehicles are also known for their strong build quality and reliability, which helps keep long-term maintenance and repair costs manageable. The Forester’s robust design and excellent visibility also contribute to its favorable risk profile with insurers, offering a compelling blend of utility and affordable ownership costs.

Nissan Kicks

The Nissan Kicks stands out as a subcompact SUV that frequently appears on lists of cars with affordable insurance. Its small engine, modest performance, and emphasis on fuel economy align with a low-risk driving profile. The Kicks is also equipped with a respectable suite of safety features for its class, contributing to its favorable standing in crash tests. Its relatively low purchase price also implies lower replacement costs for insurers in the event of a total loss. Furthermore, Nissan’s widespread service network and readily available parts help keep repair costs in check, making the Kicks an attractive option for budget-conscious buyers concerned about ongoing insurance expenses.

Chevrolet Trax

Another strong contender in the subcompact SUV segment for low insurance costs is the Chevrolet Trax. Similar to the Nissan Kicks, the Trax offers a practical, economical package without excessive power or luxury features that might drive up premiums. It often comes equipped with essential safety features, and its straightforward design typically results in reasonable repair costs. The Trax appeals to a demographic that values efficiency and affordability, which generally translates to lower perceived risk by insurance companies. Its widespread availability and established service network also ensure that parts and expertise for repairs are accessible, contributing to its economical insurance profile.

Beyond the vehicle: Driver factors and policy tips for savings

While selecting a vehicle known for low insurance premiums is a crucial step in managing your total cost of ownership, it’s important to recognize that the car itself is only one piece of the puzzle. Numerous other factors, primarily related to your driving habits and the specifics of your insurance policy, can significantly influence your annual premiums. Even if you choose one of the cars that typically answers the question of what cars have the cheapest insurance, neglecting these personal and policy-related elements could still result in higher-than-necessary costs. DoctinOnline always advocates for a holistic approach to vehicle ownership, where careful consideration of both the car and your personal circumstances leads to optimal financial outcomes.

Driver profile and history

Your personal driving record is arguably the most significant determinant of your insurance rates. A clean driving history, free of accidents, traffic violations, or DUIs, signals a low-risk driver to insurers, invariably leading to lower premiums. Conversely, a history of claims or infractions will significantly increase your rates, as it indicates a higher likelihood of future incidents. Your age, marital status, and even your credit score (in some states) can also play a role, as these demographic and financial indicators are used by insurers as proxies for risk assessment. Young, inexperienced drivers typically face higher premiums, while older, more experienced drivers with good records often enjoy more favorable rates.

Coverage options and deductibles

The type and amount of coverage you choose have a direct impact on your premiums. Opting for minimum state-required liability coverage will always be chea, but it leaves you vulnerable to significant out-of-pocket expenses in the event of an accident or other damage to your vehicle. Raising your deductible the amount you pay out of pocket before your insurance coverage kicks in is a common strategy to lower your premiums. While a higher deductible means more personal financial exposure in a claim, the reduced monthly cost can be substantial over time. It’s crucial to strike a balance between affordability and adequate protection based on your financial situation and risk tolerance.

Discounts and bundling

Most insurance providers offer a variety of discounts that can help reduce your premiums. These can include multi-policy discounts (bundling car insurance with home or renter’s insurance), good student discounts, anti-theft device discounts, low mileage discounts, and even discounts for completing defensive driving courses. It’s always worth inquiring about all available discounts when obtaining quotes. Additionally, some insurers offer telematics programs, where a device monitors your driving habits (speed, braking, mileage) and rewards safe drivers with lower rates. Proactively seeking out and applying for these discounts can significantly impact what cars have the cheapest insurance ultimately costs you personally.

Maintenance and longevity: Impact on long-term value

When discussing what cars have the cheapest insurance, it’s crucial to extend our analysis beyond just the initial premium. The true cost of vehicle ownership is a multi-faceted equation that encompasses purchase price, fuel consumption, depreciation, and critically, maintenance and repair expenses over the car’s lifetime. Vehicles that are reliable and easy to maintain not only save you money on mechanics’ bills but also tend to hold their value better, indirectly influencing insurance costs over time. A car with a proven track record of durability and low running costs presents a lower overall risk to insurers due, in part, to its extended service life and consistent performance. DoctinOnline stresses that long-term value is a key metric in assessing a vehicle’s true economic efficiency.

Scheduled maintenance costs

Regular, scheduled maintenance is essential for the longevity and safe operation of any vehicle. Cars known for low maintenance costs typically require less frequent service intervals and use readily available, inexpensive parts. For instance, models with timing chains instead of timing belts often have lower long-term maintenance costs because chains typically last the lifetime of the vehicle, whereas belts require periodic, often expensive, replacement. Similarly, vehicles with straightforward fluid changes, easily accessible filters, and robust suspension components will generally be chea. These predictable and manageable maintenance expenses contribute to a vehicle’s overall affordability and its appeal to insurers, as a well-maintained car is less likely to experience unexpected breakdowns that could lead to claims.

Expected lifespan and depreciation

The expected lifespan and depreciation rate of a vehicle significantly impact its long-term value. Cars built with robust engineering and high-quality materials tend to last longer, providing more years of service and amortizing their initial cost over a greater period. Vehicles that depreciate slowly retain more of their value over time, which means that in the event of a total loss, the payout, reflecting their enduring quality and lower long-term ownership costs. This sustained value is an important consideration when evaluating what cars have the cheapest insurance in the context of overall financial wisdom.

Conclusion

Navigating the automotive market for a new vehicle requires a keen understanding of both upfront costs and long-term financial implications. For those asking what cars have the cheapest insurance, the answer lies not just in a list of models, but in a comprehensive analysis of vehicle characteristics, driver profiles, and policy choices. DoctinOnline has explored how factors like safety ratings, reliability, repair costs, and theft rates directly influence your premiums, highlighting practical vehicle categories like sedans, compact SUVs, and minivans as consistent performers in affordability. Remember, a clean driving record, strategic coverage selection, and leveraging available discounts are equally vital in securing the most economical insurance rates. By considering all these elements, you empower yourself to make a financially intelligent decision, ensuring your next vehicle provides not only driving satisfaction but also peace of mind regarding ongoing costs. We encourage you to utilize these insights

{kind=link}